Last week before the House Economics Committee, the Governor of the Reserve Bank made it clear that the current rise in inflation has nothing to do with wages growth. And yet he also made it clear he expects workers to bear the brunt of the cost that comes from slowing inflation.

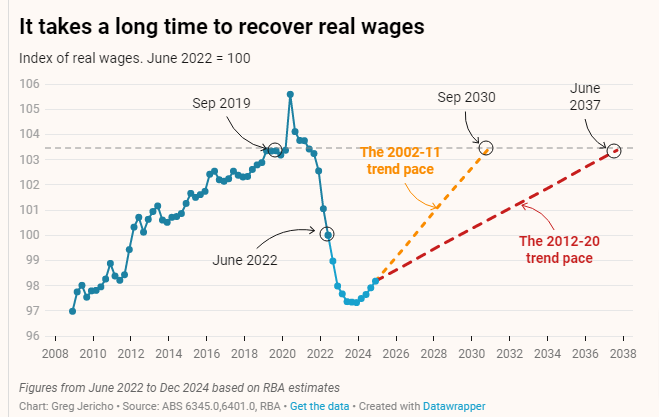

In his Guardian column, Policy Director Greg Jericho notes that given real wages have already fallen for 2 straight years any further falls will take workers’ purchasing power backwards to where it was more than a decade ago. This however is viewed as being “worse than the alternative” of inflation growth above 3%.

He notes that over the past 2 years the profit margins of many industries, and most especially the mining industry, have risen and have themselves fuelled inflation. But company profits are never expected to suffer, wages however are always viewed as either the culprit of inflation or the means to reduce it. The vast increase in mining profits, largely due to the Russian invasion of Ukraine, also highlights the urgent need for a windfall profits tax.

Using the RBA’s own estimates Jericho calcuates that by the end of next year real wages will be back at 2008 levels and even with the most optimistic outlook they will not return to 2019 levels until 2030.

The Reserve Bank’s strategy of sharply increasing interest rates risk slowing the economy into a recession even though real wages are already falling faster and for longer than they have in modern times.

You might also like

Opening statement to the ACTU Price Gouging Inquiry

This week Professor Allan Fels, the former head of the Australian Competition and Consumer Commission (ACCC), has begun an inquiry into price gouging across a range of industries, including banks, insurance companies, supermarkets, and energy providers. The inquiry commissioned by the ACTU comes off the back of the highest inflation in 30 years and the biggest falls in real wages on record.

Blame Game on Inflation has Only Just Begun

Every inflationary episode embodies a power struggle within society over who benefits from inflation, who loses out – and who will bear the cost of getting inflation back down.

Fair Work: 5.75% Award Wage Boost will not cause “Wage-Price Spiral”

Today’s 5.75% award wage increase is a necessary boost for the lowest paid workers but does not keep pace with inflation. The Fair Work Commission (FWC) has today explicitly said this increase “will consequently not cause or contribute to any ‘wage price spiral’”. Key Points: Award wage increase of 5.75% is less than inflation, which