This week the IMF released its latest World Economic Outlook. And the outlook is dire. Economic growth around the world was downgraded with recession-like conditions being predicted for many advanced economies including the USA, UK and much of the EU.

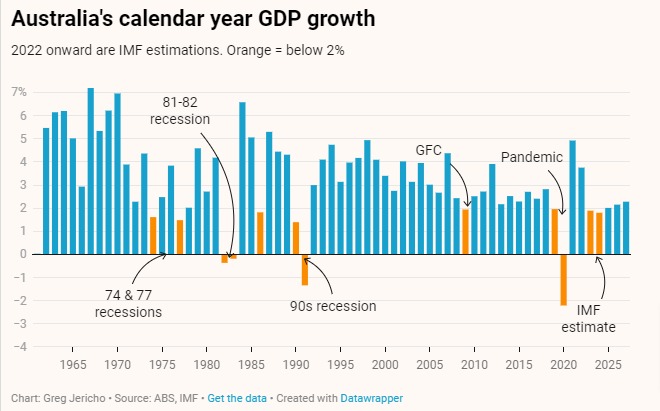

As policy director, Greg Jericho, notes in his Guardian Australia column, the outlook is not much better for Australia. The IMF is now predicting that in 2023 and 2024 Australia’s GDP will grow less than 2%. Such meagre growth in the past has been consistent with periods of recession.

The report should serve as a stark warning to central banks around the world that their efforts to limit inflation by sharply raising interest rates is becoming more and more likely to end with a recession and the resultant massive loss of jobs that will follow. Experience from the 1980s and 1990s where similar recessions followed extreme tightening of monetary policy suggests it can take a long time to reverse the damage.

While the Reserve Bank is somewhat constrained because it needs to be mindful of the rate rises in the USA that weaken the value of the Australian dollar, the IMF report should cause them to weigh much more the costs of sharply slowing growth through interest rate rises.

We know that current efforts to limit inflation growth are mostly involving workers taking a real wage hit. Having to endure rising unemployment and a recession after 2 years of already extreme falls in living standards would be disastrous, especially while profits continue to rise.

You might also like

Opening statement to the ACTU Price Gouging Inquiry

This week Professor Allan Fels, the former head of the Australian Competition and Consumer Commission (ACCC), has begun an inquiry into price gouging across a range of industries, including banks, insurance companies, supermarkets, and energy providers. The inquiry commissioned by the ACTU comes off the back of the highest inflation in 30 years and the biggest falls in real wages on record.

Blame Game on Inflation has Only Just Begun

Every inflationary episode embodies a power struggle within society over who benefits from inflation, who loses out – and who will bear the cost of getting inflation back down.

Profit-Price Spiral an Inconvenient Truth for Big Business: Economists

Despite a mainstream shift in the national conversation away from baseless claims of a “wage-price spiral”, some big business proponents and conservative economists appear unwilling to accept the economic evidence of a profit-price spiral.